This report analyzes three key areas of innovation in financial technology: mobile services, the emergence of artificial intelligence, and mechanisms of open/embedded finance. These factors are leading to the creation of a new ecosystem in which banks are transforming into technology platforms, and financial services are becoming an integral part of everyday digital experiences. The report assesses the impact of technological changes on business models and customer experience, and also addresses issues related to security and user trust.

The banking sector is undergoing a systemic transition comparable in scale to the shift that occurred about 20 years ago when people moved from paper statements to online banking. Today’s transformations are more complex: not only are new service delivery channels emerging, but the dynamics of interaction between banks, clients, and external companies are also being redefined.

Three key areas play a central role in these processes. The first is mobile services, which are currently the primary channel for accessing banking services. The second is artificial intelligence, which is being integrated into analytics, security, and personalization processes. The third involves open and embedded financial models, which are redefining the very design of banking products. Together, these elements are forming a new ecosystem in which banks are increasingly becoming technology platforms, and financial services are becoming an integral part of daily digital life.

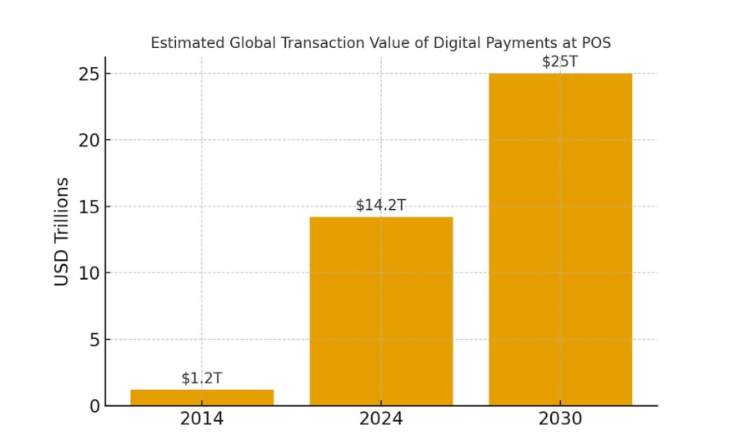

Pic. 1 — Estimated Global Transaction Value of Digital Payments at POS (2014–2030).

Mobile Solutions and Artificial Intelligence as the New Foundation of Customer Experience

Over the past decade, smartphones have become the dominant tool for managing finances—for both businesses and individuals. Major banking institutions are embracing a “mobile-first” approach, where core products are launched directly within mobile applications rather than through traditional online banking portals. For customers, this means one-click access to services; for banks, it means competing on the basis of user interfaces, speed, and convenience.

It is important to understand that mobile channels have gone far beyond their original role as mere add-ons to offline infrastructure. For a significant number of clients, the mobile app has become the only means of interacting with the bank. As a result, meticulous attention to detail—from response time to screen design—has become strategically important. Mistakes that might once have gone unnoticed on web platforms now attract immediate criticism on mobile and can directly affect customer loyalty.

Alongside the expansion of mobile channels, the adoption of artificial intelligence (AI) is gaining strong momentum. Its application extends far beyond chatbots and customer support tools. Today, AI is being used to develop scoring models, predict customer behavior, detect suspicious transactions, and combat fraud. By leveraging machine learning algorithms, financial institutions are analyzing datasets previously considered impossible to process in real time. This capability enables them to speed up credit decision-making, offer personalized products directly to clients, and manage operational risks more effectively.

One particularly compelling area is AI’s impact on risk management. Traditional methods relied on static rules, which limited their effectiveness in the face of constantly evolving fraud schemes. Machine learning algorithms can detect anomalous behavior patterns and respond before significant damage occurs. At the same time, personalization is advancing: customers are now offered not just standard pricing plans, but service packages tailored to their financial behavior.

This has notable social implications. In low-income countries around the world, mobile connectivity is increasingly becoming a tool for economic inclusion. All that is required to access payments, loans, and insurance is a smartphone and basic internet access. From a business perspective, this creates new market opportunities, while for society, it serves as a means of bridging divides between different social groups.

Open and Embedded Financial Services: A New Paradigm for the Financial Market

While artificial intelligence and mobile services have significantly enhanced the quality of user interaction, it is open and embedded finance that are ultimately reshaping the very nature of financial services.

The open finance model is based on the concept of open APIs (application programming interfaces): banks provide access to data and financial services for third-party companies, which can then develop their own solutions. As a result, a market emerges in which the boundaries between traditional financial institutions and fintech companies are increasingly blurred. Banks are no longer exclusive providers of financial services; instead, they become platforms for partners, enabling the creation of added value for end customers.

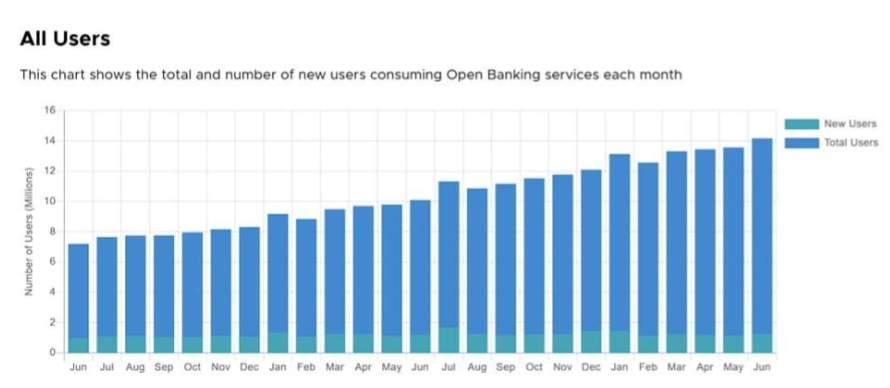

Pic.. 2 — All Users: Total and New Users of Open Banking Services (UK, 2024–2025).

Embedded Financial Services Go Beyond Traditional Boundaries

Embedded finance integrates financial solutions into non-financial products; for example, payments are processed directly within a ride-hailing app, loans are offered at the point of purchase on an e-commerce platform, and insurance is sold during travel bookings. As a result, users remain within a single digital environment, making the financial service effectively “invisible” to them.

This approach is simultaneously transforming business models across industries. Retailers and e-commerce companies can offer added value to customers and increase average transaction value, while banks gain access to new audiences without high customer acquisition costs. In fact, financial products are now being distributed according to the same principles as IT services: through partner ecosystems and platforms.

For consumers, this means significantly easier access to services. Where lending or insurance was once associated with lengthy processes, today everything can be done in just a few clicks through a familiar interface. However, with convenience comes rising expectations for transparency: users want to clearly understand who is providing the serviceand how their data is being handled.

This evolution brings not only opportunities but also new challenges for banks. They must redesign their system architectures, ensure the reliability of their API interfaces, and find the right balance between cooperation and competition. Ultimately, only those players who can seamlessly integrate into broader ecosystems—while maintaining high service quality and robust security—will emerge as long-term leaders.

The Evolution of Financial Technologies: A Three-Way Transformation

The evolution of financial technologies is moving not in one or two, but in three distinct directions: mobile services, artificial intelligence, and open/embedded finance. Each of these areas is important in its own right, but together they provide a comprehensive picture. The customer experience is becoming faster and more convenient, businesses are gaining new opportunities for growth, and the financial system as a whole is becoming more distributed and flexible.

At the same time, there are critical issues that must not be overlooked. As artificial intelligence becomes more widespread, the need for algorithmic transparency grows. As open finance becomes more widely adopted, concerns about data security intensify. And as embedded finance rapidly evolves, it becomes increasingly difficult to maintain customer trust, especially among users who may not be directly aware of which financial institution is behind the service.

In the coming years, these issues will determine which organizations become market leaders. Companies whose financial institutions can combine technological innovation with accountability and openness will earn the right to become key players in tomorrow’s digital economy. Those that respond slowly to change risk jeopardizing not just their user base, but their position in the competitive marketplace as well.

Sosin Vitalii, iOS Senior Software Engineer of FinTech industry

Sources

- Worldpay (FIS), Global Payments Report 2025, March 2025. Available at: https://worldpay.globalpaymentsreport.com/en/

- Open Banking Limited, Latest News & Updates, July 2024 – March 2025. Available at: https://www.openbanking.org.uk/about-us/latest-news/

- Bain & Company, Embedded Finance: What It Takes to Prosper in the New Value Chain, 2022. Available at: https://www.bain.com/insights/embedded-finance-opportunities/

- McKinsey & Company, The State of AI in 2024: Generative AI’s Second Year, October 2024. Available at: https://www.mckinsey.com/capabilities/quantumblack/our-insights/the-state-of-ai-in-2024